Navigating the Poseidon of Higher Interest Rates: Strategies for Community Banks

At the December 13, 2023 meeting of the Federal Open Market Committee, the Federal Reserve Bank voted to hold the benchmark Fed Funds rate between 5.25% and 5.5%. As every banker knows, rates have been rising since 2020. These increasing interest rates jab banks and bankers in three key areas: debt service coverage, collateral values, and net interest margins, creating a potential Poseidon of pain for Community Banks and bankers.

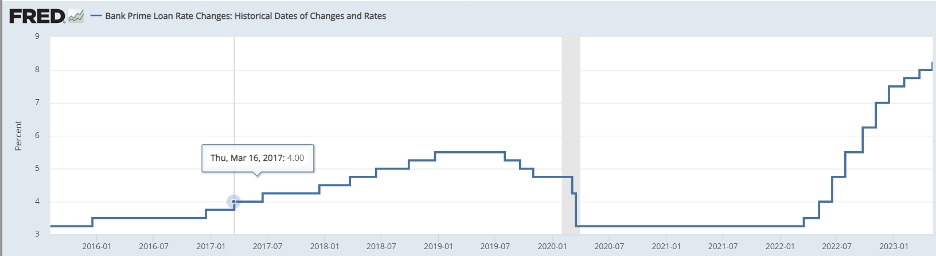

Historical Perspective: Banking has enjoyed over a decade of near-zero interest rates. Since the Fed Funds rate began tracking, rates have never been this low for this long. Only once since WW II have rates dropped below 1% (May, June, and July 1958). As the graph below shows, interest rates remained below 1% for almost 8 years before beginning a dizzying rise.

In response to the Great Recession’s economic stagnation, the Fed began dropping rates in July 2007 when the Fed Funds rate stood at 5.25%. The rate decreases continued until December 2008 when rates hit .15% or almost zero. They remained near zero until November 2015 when rates began a short period of increases that peaked at 2.4% in January 2019. By July 2019, the Fed had changed course and quickly began dropping rates.

Almost immediately, the Fed Funds rates dropped to .05%. They flatlined at just above zero until the Fed began rate tightening in February 2022. A steady series of rate hikes has resulted in the current 5.25-5.05% range. Comments by the Fed indicated that future rate hikes might be on the table. Bankers have not seen the end of rate hikes and the effects of higher interest rates yet.

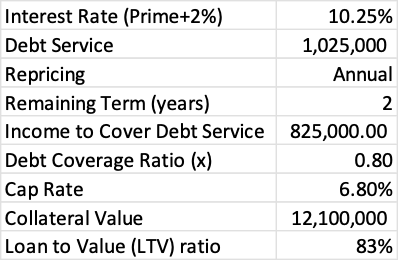

Poseidon’s Prongs One and Two – Increasing Interest Rates Wallop Loan Quality: Assume a bank underwrites and originates a loan secured by commercial real estate with these key underwriting factors:

This looks like a safe, well-underwritten loan with a nice debt coverage ratio and adequate collateral to secure the debt. And that Net Interest Margin is plump as the bank is paying little to attract deposits and borrowing costs are near zero.

Now let’s look at what happens to this loan when interest rates increase. First, like all interest rates, Prime has floated up to 8.25% as the Fed has used its “blunt instrument” — increasing interest rates – to fight inflation.

So what would fresh underwriting show?

For model purposes, we’ve kept Income to Cover Debt Service constant as, while the cash flow streams (rents) may have increased, increases in rent rates were likely offset by increased operating costs. The Cap Rate increased modestly and reflects only a few basis points above the higher band of Commercial real estate cap rates.

In the first prong of Poseidon’s fork, the loan’s interest rate has almost doubled while debt service coverage has plummeted to .8x. The property no longer supports the debt. Collateral value is the second prong of Poseidon’s fork. While the collateral still supports the debt, the value has fallen and it may soon (with further rate increases looming) be difficult to refinance the property in an amount sufficient to fully repay the existing debt.

Poseidon’s Third Prong: Banks and Bankers haven’t had to pay much for deposits in almost 15 years. Now rates are rising, and bankers must fight fire with fire, pumping up liability rates to maintain and attract new deposits. CD rates — yes, time deposits, as we called them — are coming back into vogue and rates are now above 5%. That’s a long way from the 12% plus CDs banks were forced to issue in the 1980s, but it’s well above the nearly free deposits banks had until recently.

Strategies for Community Banks:

- Proactive Portfolio Management: Regularly assess loan portfolios to identify potential risks and take corrective action early. Engage borrowers to discuss loan modifications, such as extending amortization periods or adjusting payment structures, to maintain debt service coverage.

- Stress Testing: Conduct stress tests to evaluate the impact of various interest rate scenarios on loan performance and collateral values. Use these insights to inform underwriting standards and portfolio management decisions.

- Diversification: Diversify loan portfolios across industries, geographies, and loan types to mitigate concentration risk. Consider participating in loans originated by other institutions to expand diversification opportunities.

- Deposit Strategies: Develop targeted deposit campaigns to attract and retain core deposits. Offer competitive rates on CDs and other deposit products, while emphasizing the value of long-term relationships and personalized service.

- Loan Participation Automation: Leverage loan participation automation platforms, such as Participate, to efficiently manage loan portfolios, reduce risk, and ensure compliance. These tools streamline the loan participation process, enabling community banks to collaborate with like-minded institutions and access a broader pool of lending opportunities.

Conclusion: Banks are being pummeled with credit and deposit issues caused by increasing interest rates. Contact Participate today to see how our patented end-to-end platform helps address risk and foster compliance within your loan portfolio. Email us at sales@participateloan.com or call 501.246.5148.