Loan Processing Workflow Automation: How Modern Banks Reduce Errors, Delays, and Back-Office Load

Learn how loan processing workflow automation cuts errors, speeds approvals, and modernizes banking operations across commercial and consumer lending.

Introduction

Loan processing has always been one of the most operationally heavy parts of banking — scattered documents, manual checklists, inconsistent workflows, and handoffs that slow everything down. Even with significant investment in LOS platforms, many institutions still deal with bottlenecks that eat up staff capacity and delay funding.

That’s where loan processing workflow automation comes in. By replacing manual steps with streamlined, rules-based automation, banks can move faster, reduce errors, and create a more scalable lending operation.

But there’s a deeper opportunity here too: automation doesn’t need to end at origination. Banks can extend the same efficiency gains into loan sales, participations, syndications, and post-sale servicing — where even more manual work often hides.

This article breaks down how workflow automation transforms loan processing from end to end, and how forward-thinking banks are using it to free capacity, reduce risk, and create more liquidity.

Key Takeaways

- Loan processing workflow automation reduces errors and bottlenecks across underwriting, documentation, and servicing handoffs.

- Banks still rely on manual work for post-sale servicing (participations and syndications), an area ripe for automation.

- Automation increases speed-to-close, improves borrower experience, and frees staff to focus on higher-value work.

- Integrating LOS automation with post-sale tools creates a true end-to-end digital lending lifecycle.

- Participate fills the gap after loan sale, automating the post-sale processes most banks still do manually.

Want to eliminate manual work after the loan is sold?

Explore how Participate automates post-sale servicing across participations and syndications.

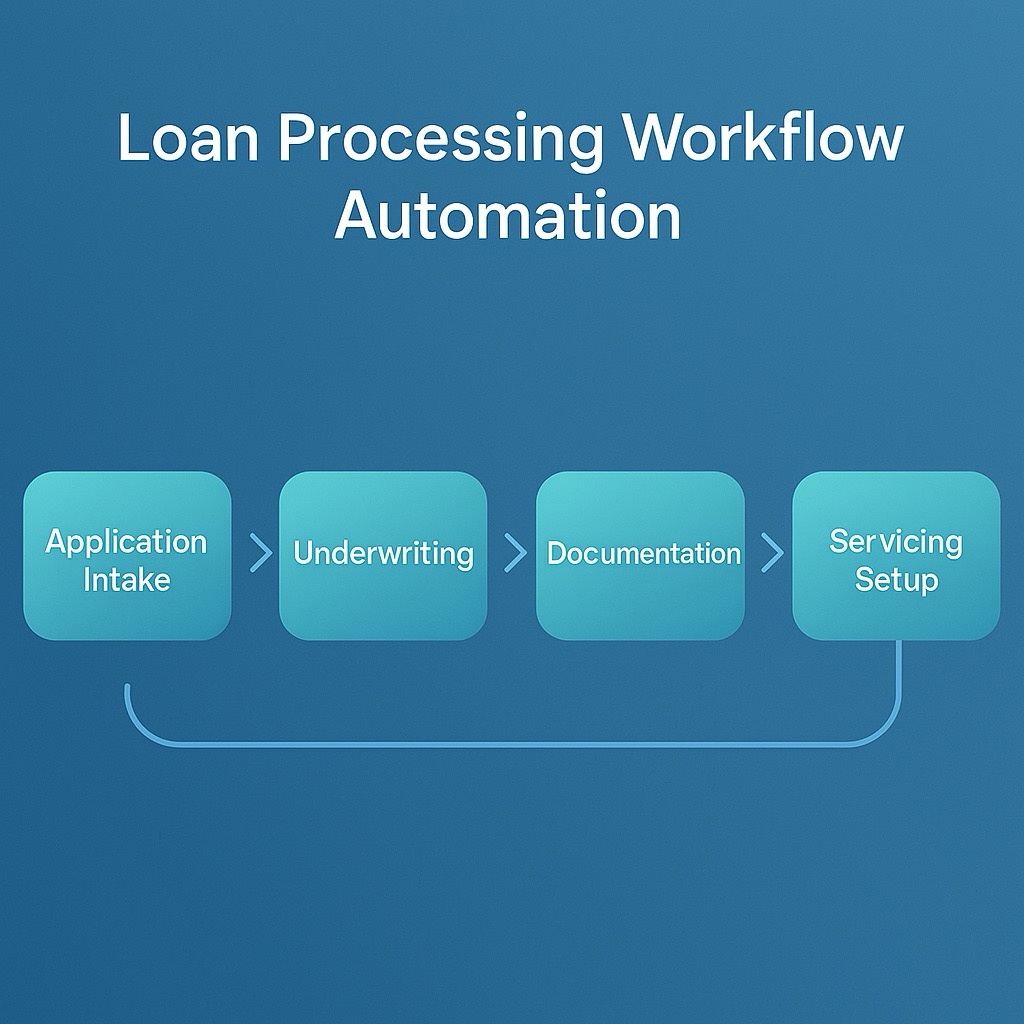

What Is Loan Processing Workflow Automation?

Loan processing workflow automation refers to the use of digital tools that guide each required step in the lending process, ensuring consistency, accuracy, and speed. Instead of manually handing off tasks between underwriting, credit, loan ops, and servicing, workflows automatically:

- Assign tasks

- Generate reminders

- Route documents

- Validate completeness

- Trigger internal approvals

- Ensure compliance steps are followed

Automation creates a single, unified process — not a collection of checklists scattered across departments.

Why Banks Are Prioritizing Workflow Automation Now

1. Rising operational burdens

Lenders are being asked to originate more volume without adding headcount. Manual processes simply don’t scale.

2. Compliance pressure

Regulators expect accurate documentation, clear audit trails, and consistent underwriting practices.

3. Talent strain

Experienced staff retire faster than banks can replace them, leaving tribal knowledge gaps filled with spreadsheets.

4. Profitability demands

Efficiency is now a direct contributor to ROA and ROE — every hour saved helps preserve margin.

Where Workflow Automation Delivers the Biggest Impact

Streamlining the Origination Process

Automation improves the way banks manage:

- Document collection

- Verification steps

- Underwriting checklists

- Exception handling

- Approval routing

- Compliance steps

Expert Tip:

Banks that standardize workflows see 20–40% faster decisioning times without sacrificing credit quality.

Cleaning Up the Servicing Handover

Once a loan closes, workflow automation ensures correct and consistent steps, including:

- Boarding to core

- Tickler setup

- Payment schedules

- Escrow setups

- Insurance and tax verification

Even small mistakes here cause significant downstream rework.

Reducing Errors Across Departments

Manual process pain points often include:

- Duplicate data entry

- Missing documents

- Inconsistent underwriting exceptions

- Delayed servicing corrections

- Miscommunication between teams

Automation fixes these by enforcing exact required steps.

But There’s a Major Gap: Post-Sale Loan Workflow Automation

Even banks with excellent LOS systems and strong servicing workflows still rely on manual work when a loan (or portion of it) is sold.

Problem: automation usually stops when the loan is sold

For participations and syndications, most banks still use:

- Spreadsheets

- Email chains

- Shared drives

- Manually constructed reports

- Phone calls when balances don’t match

This is the ironic truth:

Banks who automate everything before the sale go right back to spreadsheets after the sale.

Why Post-Sale Loan Processing Needs Automation Too

Every payment becomes manual work

When multiple participants own shares of a loan, someone must:

- Split principal & interest

- Track daily rate changes

- Notify participants

- Reconcile balances

- Push documents

- Maintain audit trails

Every misstep introduces risk.

Banks lose time and capital

Manual post-sale work:

- Slows down loan sale cycles

- Creates reconciliation delays

- Drains staff capacity

- Limits liquidity

- Prevents lenders from taking new opportunities

Automation accelerates everything.

Executive visibility suffers

Without automated reporting, executives struggle to see:

- Exposure

- Concentration risk

- Loan partner activity

- Liquidity impact

- Real-time balances

Automation centralizes all reporting.

How Participate Fits Into the Automated Workflow

Participate extends automation beyond origination and core servicing into the area banks need most: post-sale servicing.

With Participate, banks automate:

- Post-sale funding and payments

- Rate changes and notifications

- Shared balance tracking

- Document exchange

- Participant reporting

- Audit trails

- Ongoing servicing obligations

It plugs directly into the bank’s existing workflows:

- LOS → Participate → Core

Benefits of Extending Workflow Automation to Loan Sales

1. Faster deal execution

Participations and syndications move in hours, not weeks.

2. Stronger liquidity management

Free capital faster → fund more deals → grow earning assets.

3. Improved risk management

Real-time shared balances reduce exposure surprises.

4. Staff efficiency

One analyst can manage 10× the servicing volume.

5. Increased fee income

Servicing fees (25 bps common) become a predictable revenue stream.

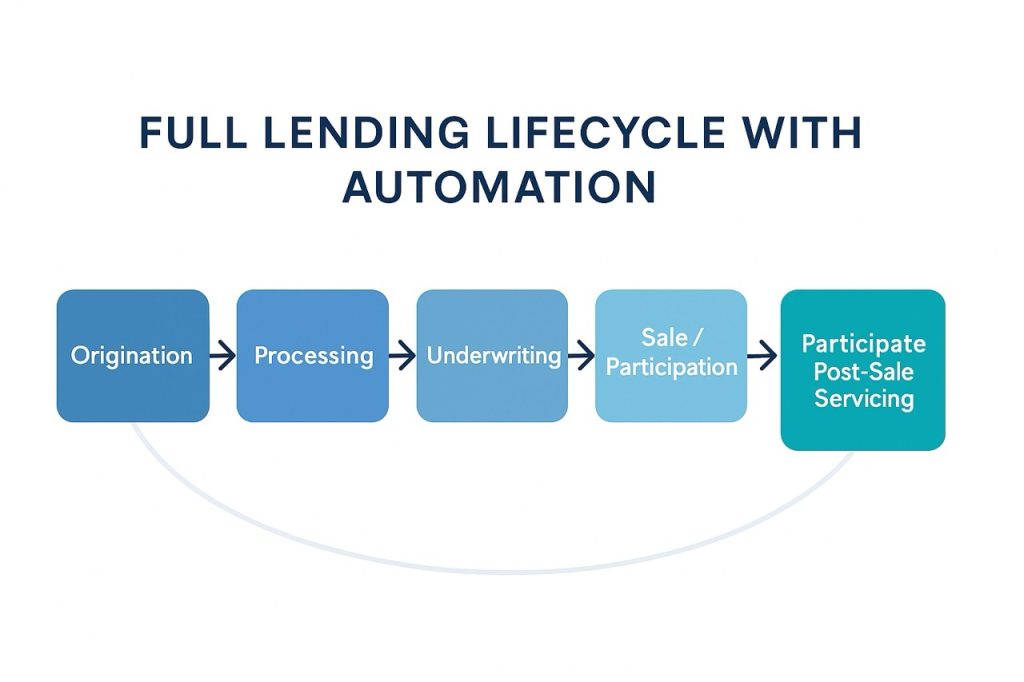

How To Connect LOS Automation With Post-Sale Automation

Banks create an end-to-end lifecycle by:

- Automating origination and underwriting

- Automating boarding and servicing setup

- Automating loan sale workflows

- Automating downstream servicing with Participate

This creates a continuous loop that strengthens liquidity, efficiency, and scalability.

FAQ Section

1. Does loan workflow automation replace our LOS?

No — it enhances it. LOS handles origination, while Participate automates post-sale servicing.

2. Can automation reduce manual post-sale reconciliation?

Yes. Participate virtually eliminates out-of-balance issues through shared real-time data.

3. Do we need new staff to adopt automation tools?

No — automation reduces staffing pressure, not increases it.

4. Will automation help manage concentration risk?

Yes. Faster loan sales + automated reporting make risk management significantly easier.

5. Does Participate integrate with our core and LOS?

Yes — Participate integrates with major LOS platforms (like nCino) and core systems (Fiserv, FIS, Jack Henry).

Conclusion

Loan processing workflow automation is no longer optional. Banks that adopt modern workflow tools move faster, reduce errors, and improve operational capacity. But the biggest gains come when automation doesn’t stop at the sale — when the entire lifecycle, from origination to post-sale servicing, becomes seamless.

Participate closes that final gap, helping banks transform the most manual and overlooked part of loan processing into a streamlined, automated engine for liquidity and growth.

Ready to automate the most manual part of loan processing?

See how Participate transforms post-sale servicing for participations and syndications.