What Is Loan Syndication? A Complete Guide for Banks and Financial Institutions

A $25 million commercial real estate deal lands on your desk. The borrower is strong. The underwriting works. The relationship matters.

But there’s a problem: holding the entire credit would push your institution past internal concentration limits—or at least uncomfortably close. Passing on the deal isn’t ideal. Neither is overexposure.

This is the moment many Chief Lending Officers face: how to say “yes” to the borrower without compromising the balance sheet.

Loan syndication exists precisely for this scenario.

What Is Loan Syndication?

Loan syndication is a financing structure in which multiple lenders jointly originate and fund a single loan, typically at origination, with one institution acting as the lead arranger and administrative agent.

Unlike secondary transactions, syndication happens upfront. The loan is structured, underwritten, and distributed across multiple institutions before—or at—the time of closing. Each lender holds a direct share of the credit, governed by a common credit agreement.

Syndication is most commonly used for:

- Large commercial loans (CRE, C&I, project finance)

- Credits exceeding a single bank’s lending limit

- Situations requiring diversified risk across institutions

- Complex facilities (multi-tranche, revolving + term structures)

The structure allows banks to participate in larger deals while maintaining prudent risk exposure and regulatory compliance.

Key Takeaways

- Loan syndication enables banks to fund larger deals while managing concentration and lending limits.

- The lead arranger controls structuring, underwriting, and distribution, while participants fund portions of the loan at origination.

- Syndication differs materially from participation and whole-loan sale, especially in timing, control, and borrower relationship.

- Operational complexity is real—documentation, servicing, and communication across lenders can introduce risk without the right infrastructure.

- Technology is reshaping syndicated lending, improving speed, transparency, and scalability across the lifecycle.

See It in Practice

See how Participate supports the syndicated loan lifecycle

How Loan Syndication Works

The Core Structure

At its simplest, syndicated lending involves three primary roles:

- Lead Arranger (or Bookrunner):

Structures the deal, underwrites the credit, and distributes portions to other lenders. - Administrative Agent:

Manages ongoing servicing—payments, reporting, covenant tracking. - Participant Lenders (Syndicate Members):

Fund portions of the loan and share in risk and return.

In many community and regional bank scenarios, the lead and agent are the same institution.

Step-by-Step Process

- Origination & Structuring

- Lead bank negotiates terms with borrower

- Defines facility structure, pricing, covenants

- Underwriting

- Lead performs credit analysis

- Prepares offering materials (credit memo, CIM)

- Syndication / Distribution

- Loan is marketed to potential lenders

- Commitments are gathered

- Allocation & Documentation

- Final lender group is set

- Legal agreements executed

- Closing & Funding

- Each lender funds its portion

- Loan closes as a single facility

- Ongoing Administration

- Agent manages payments, reporting, compliance

When to Use Loan Syndication

Syndication is most appropriate when:

- The loan size exceeds legal lending limits

- A bank wants to retain a relationship but reduce exposure

- The credit is complex or multi-structured

- There is strong market demand from other lenders

It is less suitable when:

- Flexibility post-closing is required (participations are more flexible)

- Speed and simplicity outweigh structure

- The loan is small relative to operational overhead

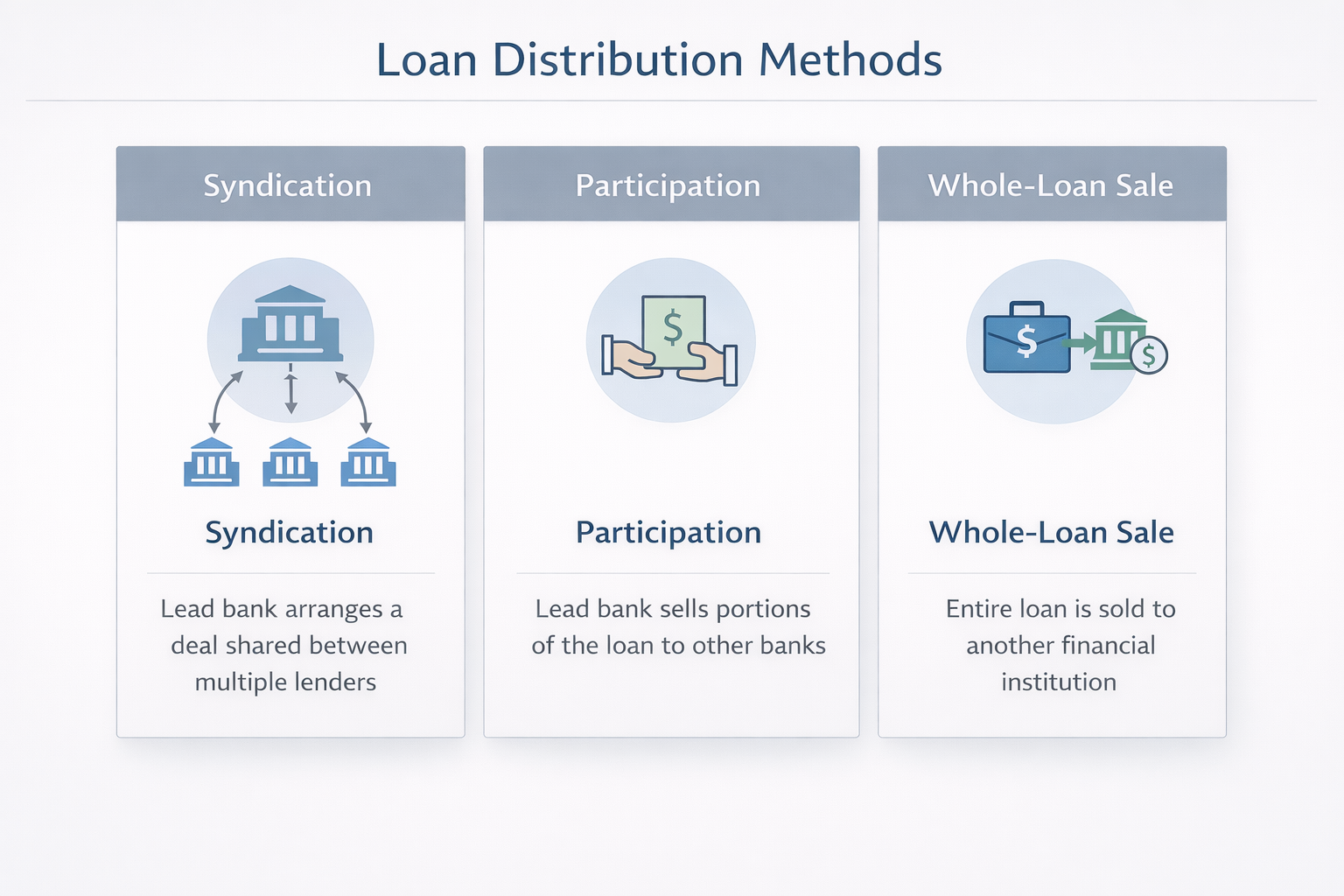

Loan Syndication vs. Participation vs. Whole-Loan Sale

These three structures are often grouped together—but they serve different strategic purposes.

Comparison Table

| Feature | Loan Syndication | Loan Participation | Whole-Loan Sale |

|---|---|---|---|

| Timing | At origination | After origination (or at closing) | After origination |

| Structure | Multiple lenders fund directly | Lead sells portions of loan | Entire loan transferred |

| Borrower Relationship | Shared but led by arranger | Retained by originating bank | Transferred to buyer |

| Control | Lead arranges; shared governance | Originator retains control | Buyer assumes control |

| Documentation | Syndicated credit agreement | Participation agreement | Loan assignment |

| Flexibility Post-Close | Limited | High | N/A (ownership transferred) |

| Use Case | Large/complex deals | Balance sheet optimization | Liquidity / exit strategy |

Practical Guidance

- Use syndication when structuring large deals from day one.

- Use participation when managing exposure dynamically over time.

- Use whole-loan sales when exiting a position entirely.

No structure is inherently “better.” The right choice depends on:

- Timing

- Strategic intent

- Operational capacity

- Risk appetite

Benefits of Loan Syndication

1. Expanded Lending Capacity

Syndication allows banks to participate in deals that would otherwise exceed internal or regulatory lending limits.

2. Risk Diversification

Exposure is spread across institutions, reducing concentration risk across:

- Borrowers

- Industries

- Geographies

3. Relationship Retention

The lead bank maintains the borrower relationship—even when holding a smaller share.

4. Fee Income Opportunities

Lead arrangers generate:

- Structuring fees

- Syndication fees

- Agency/servicing fees

5. Market Signaling

Participating in syndicated deals can enhance:

- Market credibility

- Institutional relationships

- Access to future opportunities

Risks and Considerations

Syndicated lending introduces complexity that must be actively managed.

Credit Risk

Shared exposure does not eliminate risk—only distributes it. Each lender must independently assess credit quality.

Operational Risk

Manual processes—spreadsheets, email-based workflows—can create:

- Reconciliation errors

- Delayed payments

- Data inconsistencies

These risks are well documented in traditional loan participation and syndication processes, where manual workflows introduce inefficiencies and communication gaps.

Agency Risk

Participants rely on the lead/agent for:

- Reporting accuracy

- Covenant monitoring

- Servicing execution

Liquidity Risk

Syndicated loans are less liquid than traded securities. Secondary market exits can take time.

Legal & Documentation Complexity

Multi-party agreements increase:

- Negotiation time

- Legal costs

- Ongoing coordination requirements

Regulatory Considerations

Loan syndication operates within well-established regulatory frameworks, but several areas require attention:

1. Lending Limits

Syndication is commonly used to comply with:

- Legal lending limits (12 CFR Part 32 for national banks)

2. Risk Management Expectations

Regulators expect banks to:

- Underwrite syndicated loans as if held individually

- Maintain independent credit analysis

(OCC and FDIC guidance emphasize this standard)

3. Interagency Guidance (SR 14-3)

The Federal Reserve’s guidance on leveraged lending (SR 14-3) highlights:

- Underwriting discipline

- Risk rating consistency

- Portfolio monitoring

4. Anti-Kickback / Fee Transparency

Fee structures in syndications must be:

- Transparent

- Properly disclosed

- Free of conflicts of interest

5. Risk Retention

While Dodd-Frank risk retention rules primarily target securitizations, the principle applies:

- Lead banks should maintain “skin in the game” to align incentives

The Role of Technology in Loan Syndication

Syndicated lending has historically been operationally heavy.

Manual workflows—email, spreadsheets, fragmented systems—introduce:

- Delays

- Errors

- Limited transparency

What’s Changing

Modern syndicated lending increasingly relies on:

- Digital workflows

- Standardized documentation

- Real-time data sharing

Automation platforms enable:

- Faster deal distribution

- Improved participant communication

- Streamlined servicing and reporting

These platforms reduce time to close and improve data consistency across institutions, while enabling better balance sheet management and liquidity optimization.

Where Technology Adds the Most Value

1. Deal Distribution

- Faster syndicate formation

- Broader lender reach

2. Data Standardization

- Consistent loan data across participants

- Reduced reconciliation issues

3. Servicing Automation

- Automated payment splits

- Real-time balance tracking

4. Compliance & Reporting

- Audit-ready records

- Standardized documentation

Internal Resources

- Learn more about loan participation

- Explore loan portfolio strategies

- See servicing automation in action

Frequently Asked Questions

1. What is the difference between loan syndication and loan participation?

Loan syndication occurs at origination, where multiple lenders jointly fund a loan. Loan participation occurs after origination, where the lead bank sells portions of an existing loan while retaining control and borrower relationship.

2. How does a bank become a lead arranger?

A bank becomes a lead arranger by:

- Originating the borrower relationship

- Structuring and underwriting the deal

- Having distribution capability (relationships with other lenders)

- Demonstrating operational capacity to administer the loan

3. What are the risks of syndicated lending for smaller banks?

Key risks include:

- Over-reliance on the lead bank

- Limited visibility into borrower performance

- Operational complexity in servicing and reporting

- Exposure to unfamiliar markets or industries

Smaller institutions must ensure independent credit analysis and ongoing monitoring.

4. How long does a loan syndication typically take to close?

Timelines vary, but typical ranges:

- Middle-market deals: 2–6 weeks

- Larger or complex deals: 6–12+ weeks

Delays often stem from:

- Documentation negotiation

- Lender commitments

- Operational coordination

5. What regulatory reporting is required for syndicated loans?

Banks must:

- Report exposures in Call Reports

- Maintain internal risk ratings

- Track concentration limits

- Ensure compliance with OCC/FDIC guidance

Each institution must treat its portion as if it originated the loan.

Conclusion

Loan syndication is a foundational tool for modern banking. It allows institutions to say “yes” to larger opportunities while maintaining disciplined risk management.

But it is not without complexity.

The trade-off is clear:

- Greater lending capacity and diversification

- In exchange for operational and coordination challenges

For many institutions, the question is no longer whether to syndicate—but how to do it efficiently, transparently, and at scale.

See How Participate Fits Into the Syndicated Lending Lifecycle

Explore how Participate supports syndications, participations, and loan sales across the full lifecycle → Explore how Participate fits into the syndicated lending lifecycle

If this piece doesn’t just explain syndication—but helps your team make better decisions about when and how to use it—it’s doing its job.