What Is Loan Participation? A Complete Guide for Banks and Financial Institutions

A commercial lender finally wins a strong relationship—a growing borrower with a $25MM credit request. The underwriting checks out. The relationship matters. But there’s a problem: the exposure breaches internal concentration limits, pushes against legal lending limits, or simply doesn’t fit the balance sheet.

Walking away isn’t an option. Holding the full credit isn’t prudent. This is where loan participation becomes a core strategic tool—not just a workaround, but a disciplined way to keep lending while managing risk.

For community and regional banks and credit unions, loan participation has evolved from a niche practice into a foundational balance sheet management strategy. It enables institutions to serve larger borrowers, diversify portfolios, and optimize capital—all while maintaining customer relationships.

This guide breaks down exactly how loan participation works, why it matters, and how leading institutions are modernizing the process.

Key Takeaways

- Loan participation allows banks to share ownership of a loan while retaining the borrower relationship.

- It is a critical tool for managing concentration risk and lending limits, including compliance with regulatory thresholds like 12 CFR Part 32.

- Participations differ from syndications and whole-loan sales in structure, timing, and control.

- Both buyers and sellers must apply full underwriting discipline—regulators expect participations to be treated like originated loans.

- Automation is transforming participation lending, reducing operational risk and enabling scalable growth.

What Is Loan Participation?

Loan participation is the pro-rata sharing of a loan between a lead (originating) bank and one or more participating institutions. The originating bank retains the borrower relationship and services the loan, while participants own a contractual share of the credit.

Key Terms

- Originating Bank (Lead Bank): The institution that underwrites and services the loan.

- Participant(s): Institutions that purchase a portion of the loan.

- Loan Participation Agreement: The legal contract governing rights, obligations, and cash flow sharing.

- Pro-Rata Sharing: Each participant receives a proportional share of principal, interest, and fees.

At its core, loan participation allows a bank to sell down exposure without exiting the relationship—a critical distinction in relationship banking.

Participation vs. Syndication

Loan participation is often confused with syndication, but they are structurally different:

- Loan Syndication: Structured at origination with multiple lenders funding the loan simultaneously, typically led by a lead arranger.

- Loan Participation: Typically occurs after origination, where the lead bank sells portions of an existing loan.

If you want a deeper dive, see this loan syndication guide.

Participation vs. Whole-Loan Sale

- Loan Participation: Partial transfer of ownership; the originating bank retains servicing and relationship.

- Whole-Loan Sale: Full transfer of ownership; the originating bank exits the credit entirely.

Why Do Banks Use Loan Participations?

Loan participation is not just a tactical solution—it’s a strategic lever for balance sheet management.

1. Reduce Concentration Risk

Regulators consistently emphasize diversifying. Participations allow banks to reduce exposure to a single borrower, industry, or geography without declining the loan.

2. Manage Lending Limits

Under 12 CFR Part 32, national banks must adhere to legal lending limits. Participations allow institutions to stay within regulatory thresholds while still originating larger credits.

3. Diversify Geographic Exposure

Participating in loans originated by other institutions enables banks to access new markets without building local origination teams.

4. Generate Fee Income

Originating banks can earn servicing and structuring fees while sharing risk—often adding meaningful non-interest income.

5. Free Up Capital for Additional Lending

Selling down portions of loans improves liquidity and capital efficiency, enabling more originations.

How Does a Loan Participation Work? (Step-by-Step)

Understanding the lifecycle is critical for both credit and operations teams.

1. Origination

The lead bank underwrites and approves the loan, structuring it based on borrower needs and internal credit policy.

2. Decision to Participate

The bank determines it cannot—or should not—hold the full exposure due to:

- Concentration limits

- Liquidity constraints

- Risk appetite

3. Structuring the Participation

The lead defines:

- Participation percentage

- Pricing and yield

- Fee structure

- Participation agreement terms

4. Distribution to Participants

The loan is offered to other institutions—either through direct relationships or a network such as the Participate marketplace.

5. Execution and Funding

Participants commit capital and execute the participation agreement. Funds are allocated according to ownership percentages.

6. Ongoing Administration

The originating bank:

- Services the loan

- Collects borrower payments

- Distributes principal and interest pro-rata

- Provides reporting to participants

Selling vs. Buying a Loan Participation

Loan participation is a two-sided market—each side has distinct priorities.

Selling a Participation (Originating Bank)

From the seller’s perspective, the goal is to:

- Retain the borrower relationship

- Reduce exposure

- Generate fee income

- Maintain control over servicing

Modern platforms now allow banks to publish participations, manage agreements, and automate servicing workflows, replacing spreadsheets and manual processes.

Buying a Participation (Participant Bank)

For buyers, participations are a way to deploy capital and diversify portfolios.

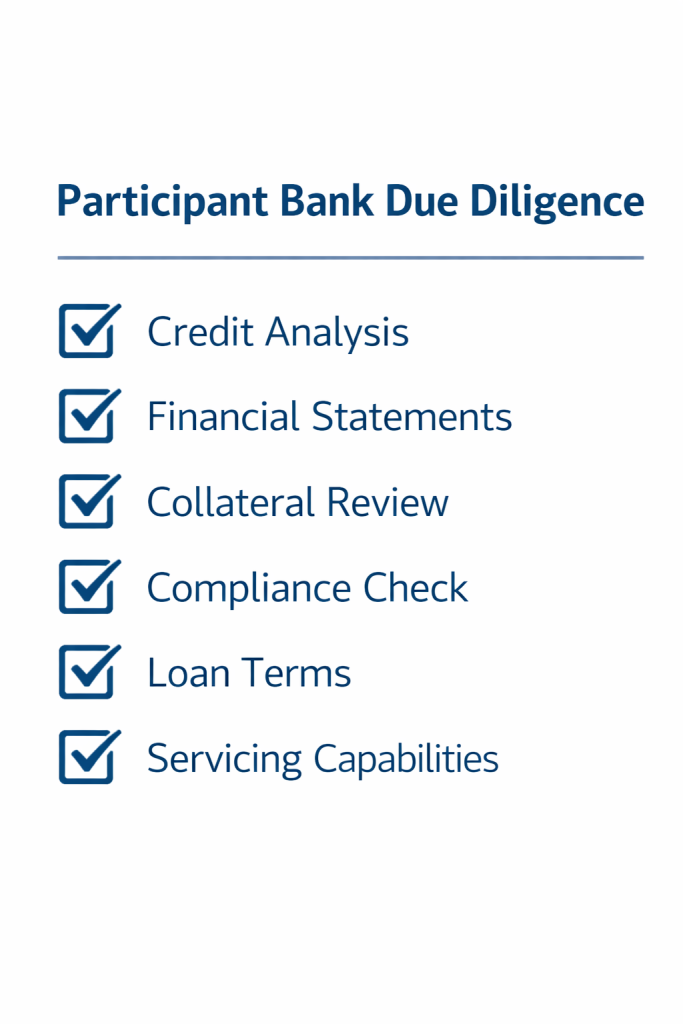

Due Diligence Checklist

Participants should evaluate:

- Credit underwriting (as if originated internally)

- Borrower financials and collateral

- Structure and covenants

- Lead bank reputation and servicing capabilities

- Participation agreement terms

Regulatory guidance from the FDIC and OCC is clear: purchased participations must be underwritten and monitored with the same rigor as originated loans.

Risks of Loan Participations

While participations offer clear benefits, they introduce risks that must be actively managed.

1. Credit Risk

The borrower may default. Participation does not eliminate credit risk—it redistributes it.

2. Operational Risk

Manual processes—spreadsheets, email-based workflows—can lead to:

- Reconciliation errors

- Payment misallocations

- Reporting delays

3. Legal and Documentation Risk

Poorly structured participation agreements can create ambiguity around:

- Loss sharing

- Decision-making authority

- Workout scenarios

4. Compliance Risk

Failure to adhere to regulatory expectations can result in exam findings. Regulators expect:

- Independent credit analysis

- Ongoing monitoring

- Proper documentation

Mitigation Strategies

- Standardized participation agreements

- Strong credit processes

- Automated servicing and reporting

- Transparent communication between participants

Automation is increasingly critical here—reducing errors, improving transparency, and strengthening compliance controls.

What to Look for in a Loan Participation Platform

As participation volumes grow, manual processes become a bottleneck. Leading institutions are adopting platforms to streamline the lifecycle.

Key Capabilities

1. Standardized Agreements

Pre-built participation agreements reduce legal complexity and accelerate deal execution.

2. Automated Payment Distribution

Automating principal and interest splits eliminates reconciliation risk.

3. Real-Time Visibility

Participants need access to:

- Current balances

- Transaction history

- Loan performance

4. Compliance Safeguards

Built-in workflows help ensure adherence to regulatory expectations.

5. Core System Integration

Integration with loan origination and core systems eliminates duplicate data entry.

Platforms that provide a shared “system of truth” for all participants significantly reduce operational risk and improve scalability.

For more on operational efficiency, see this article on loan servicing automation.

FAQ: Loan Participation

What is the difference between loan participation and loan syndication?

Loan participation involves selling portions of an existing loan, while syndication occurs at origination with multiple lenders funding the loan simultaneously.

How is a participation agreement structured?

It defines ownership percentages, payment distribution, servicing responsibilities, and rights in default or restructuring scenarios.

What regulatory rules apply to loan participations?

Guidance from the FDIC and OCC requires banks to underwrite and monitor participations as if they originated them. Lending limits (e.g., 12 CFR Part 32) also apply.

Can a borrower have both a syndicated loan and participations in the same credit?

Yes. A syndicated loan can later be participated in the secondary market.

How long does it take to set up a loan participation?

Traditionally weeks—but with modern platforms, execution timelines can be reduced significantly through automation.

What fees are typically involved?

Common fees include:

- Origination fees

- Servicing fees (often ~25 bps)

- Structuring fees

Conclusion

Loan participation has become a cornerstone of modern balance sheet management for banks and credit unions. It allows institutions to say yes to more borrowers, manage risk intelligently, and optimize capital—all without sacrificing relationships.

But the process matters. Institutions still relying on manual workflows face increasing operational risk, limited scalability, and reduced visibility. As participation volumes grow, so does the need for standardized, automated infrastructure.

The banks that are winning today are not just participating—they are systematically managing participations as a strategic function of lending, risk, and liquidity.

To go deeper on portfolio strategy, explore our guide to loan portfolio analysis.

Ready to Modernize Your Loan Participation Strategy?

See how Participate helps banks manage the full loan participation lifecycle—from origination to post-sale servicing—or talk to our team today.