How Do Banks Reduce Concentration Risk? A Practical Playbook for Banks That Want to Keep Lending

If you’re a lender or risk leader, you already know the textbook answer: set limits, monitor exposures, stress test, and diversify. The problem is that none of that helps when a great borrower is sitting across the desk and your portfolio is brushing up against policy thresholds.

So how do banks reduce concentration risk in the real world—without shrinking their business or saying “no” to relationship loans?

This guide breaks down the most practical moves banks use to reduce concentrations and keep lending, plus the operational “gotchas” most articles skip.

Key takeaways

- Concentration risk isn’t just “too much CRE”—it’s any exposure that can amplify losses across borrowers, industries, geographies, or products.

- Regulators expect banks (and credit unions) to identify, measure, monitor, and control concentrations—and treat it as connected to liquidity and interest-rate risk.

- The fastest real-world levers are typically sell-down strategies (participations/syndications/whole-loan sales) combined with disciplined limits and stress testing.

- The hidden failure point isn’t strategy—it’s operations: reporting, reconciliation, and post-sale servicing are where risk and reputational issues show up.

- The best programs pair governance (limits + monitoring) with execution capability (speedy distribution + clean servicing).

Want a simple way to quantify the upside of selling down exposure vs. holding 100%? Use Participate’s ROI Calculator and see what participation-driven liquidity and fee income could look like for your bank.

What concentration risk really means (and why it becomes a growth problem)

Concentration risk shows up when a bank’s risk is overly tied to one factor—like a single borrower relationship, an industry (CRE, healthcare, agriculture), a geography, or even a loan structure.

From a supervisory standpoint, it’s not just a “nice-to-have” concept. The OCC describes a concentration of credit as obligations exceeding 25% of a bank’s capital structure, and notes concentrations can involve a borrower/group or industry dependence.

For credit unions, the NCUA emphasizes that management has a responsibility to identify, measure, monitor, and control concentration risk, and that concentration risk should be managed alongside credit, interest-rate, and liquidity risks.

Why it becomes urgent

Concentrations tend to become painful in the same moments you want to grow:

- A sector is booming (and you’re winning deals)

- Liquidity tightens

- Rates shift and collateral values get questioned

- Examiners lean in on policy exceptions

Expert tip: Concentration risk becomes a strategy problem when you hit limits—but it becomes an execution problem when you can’t move exposure quickly enough to keep lending.

How do banks reduce concentration risk in practice?

Most online articles stop at “set tighter limits.” Real banks use a layered approach: governance + analytics + release valves that let them keep lending.

Below are five practical methods banks use most often—starting with the moves that create the fastest relief.

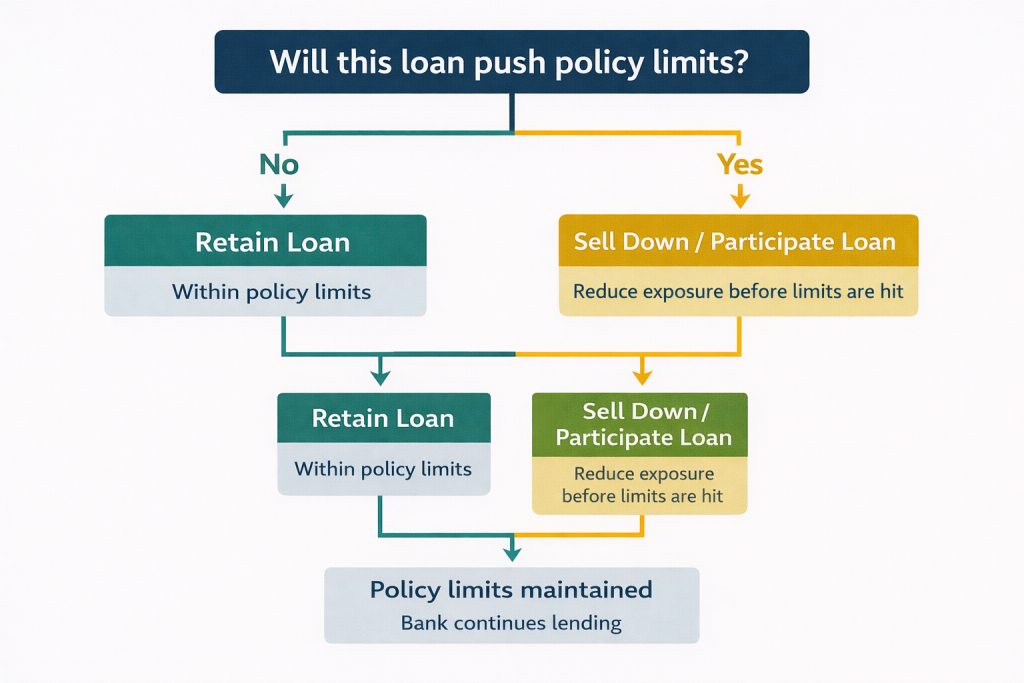

1) Sell down exposure with loan participations

If you’re near a policy limit but want to keep the borrower relationship, selling a portion of a loan is often the cleanest option.

Why participations are a go-to lever

- Immediate reduction in hold exposure (by borrower, industry, geography, etc.)

- Preserves the client relationship and fee opportunity

- Creates a repeatable playbook: originate → sell-down → service

Even regulator-adjacent commentary acknowledges participations as a way to alleviate concentrations—while still emphasizing sound underwriting and due diligence.

How to operationalize participations (quick checklist)

- Define the concentration you’re targeting (borrower / CRE subtype / geography / term)

- Identify loans eligible for sell-down (new origination and/or seasoned)

- Decide your “retain” strategy (what you keep vs. distribute)

- Pre-align legal + credit standards with your likely participants

- Build a servicing plan (who calculates/sends what, how often, and how breaks get resolved)

Did you know? A lot of “we can’t participate that” objections aren’t credit-driven—they’re ops-driven (manual notices, spreadsheets, reconciliation breaks). If you fix the ops layer, you often unlock far more participation capacity.

2) Use syndication at origination for known large exposures

Syndication is typically best when you already know the exposure will be above internal appetite at closing. Unlike a participation sell-down (which can happen pre- or post-close), syndication is often structured up front with multiple lenders.

When syndication is the right tool

- Large relationship facilities where hold limits will be exceeded at close

- Borrowers who expect a multi-bank structure

- Situations where you want a clear agent/administrative framework from day one

Common pitfall

Syndications are great structurally, but they can still bog down operationally if processes rely on emails, attachments, and manual remittance calculations. That’s where automation and a shared system of record can reduce downstream friction.

3) Execute whole-loan sales when liquidity is the primary goal

Whole-loan sales are the blunt instrument: they can reduce exposure and generate liquidity quickly, but they may come with trade-offs in relationship continuity and ongoing revenue.

Whole-loan sales fit when:

- You need balance sheet relief fast

- The relationship is less strategic or the credit no longer fits appetite

- You’re rebalancing a portfolio (e.g., reducing a segment that’s over-limit)

Expert tip: Many banks mix tools: keep the borrower via participation on core relationships, and use whole-loan sales for non-core exposures to reset portfolio shape.

4) Reduce concentrations through portfolio rebalancing and diversification

Not every concentration problem gets solved by selling. Banks also reduce concentration risk by reshaping what they originate next.

Practical diversification moves

- Adjust origination mix targets (by sector, geography, product)

- Tighten underwriting or structure (LTV, DSCR, amortization, covenants)

- Add guardrails around the fastest-growing niches

- Use stress testing and sensitivity analysis to see which segments break first

Many risk frameworks emphasize stress testing and credit review as key components of concentration risk management.

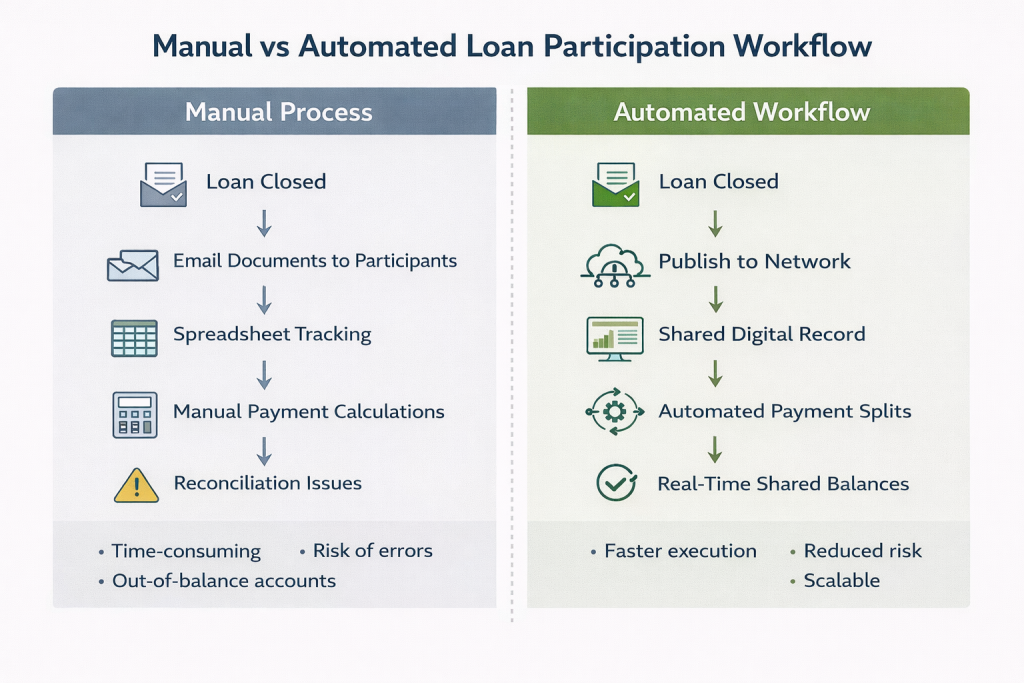

5) Fix the hidden bottleneck: operational execution (where concentration strategies fail)

Here’s the truth: a bank can have a perfect concentration policy and still be stuck, because execution takes too long.

Where banks get burned operationally

- Participant reporting is inconsistent

- Interest rate changes don’t sync across partners

- Payment splits require manual calculations

- Month-end reconciliation creates “breaks” and reputational friction

This matters because supervisors look at how well you manage concentrations in practice—not just what the policy says. The OCC’s Concentrations of Credit handbook emphasizes concentration risk management as part of overall supervisory assessment.

A simple 30–60–90 day plan to reduce concentration risk without stopping lending

If you’re close to limits and want a pragmatic plan, here’s a clean sequence:

First 30 days: clarify exposure + pick your lever

- Confirm which concentration is binding (borrower/industry/geo/product)

- Identify loans to sell-down (pipeline + portfolio)

- Decide retain targets (what you keep vs. distribute)

Next 30 days: build repeatable execution

- Standardize documents and participation terms

- Identify distribution partners (existing network + new)

- Put a servicing process in place (reporting cadence, notices, reconciliations)

Next 30 days: institutionalize and scale

- Create a “sell-down playbook” by loan type

- Automate where errors and delays occur most

- Track outcomes (limit relief, liquidity, cycle time, fee income)

FAQ

What is concentration risk in banking?

Concentration risk is the risk of outsized loss due to heavy exposure to one borrower, industry, geography, product, or correlated factor—where a single negative event can drive broad stress.

What do regulators consider a “credit concentration”?

The OCC describes concentrations of credit in supervisory materials and notes a concentration can include obligations exceeding 25% of a bank’s capital structure, among other portfolio concentration concepts.

Are loan participations a common way to reduce concentration risk?

Yes. Participations can reduce hold exposure while preserving relationships and continuing to lend. Regulator-adjacent guidance also references participations as a way to alleviate certain balance sheet concentrations when done with sound risk management.

What’s the fastest way to reduce concentration risk?

If a limit is binding today, the fastest levers are typically sell-down strategies (participations, syndications, whole-loan sales). Long-term, diversification and disciplined limits prevent recurrence.

Why do concentration-risk programs fail even with good policies?

Execution. Manual processes (spreadsheets, email-based servicing, inconsistent participant reporting) slow sell-downs and create reconciliation risk—undermining the strategy.

Conclusion

So, how do banks reduce concentration risk while still growing? They combine solid governance (limits + monitoring + stress testing) with practical release valves (participations, syndication, loan sales)—and they eliminate the operational friction that makes those tools slow, risky, or hard to scale.

If your bank is bumping into concentration thresholds and you want to keep saying “yes” to strong borrowers, the next step is building a repeatable sell-down and servicing workflow that your lending, credit, and ops teams can trust.

Final CTA: Ready to see what sell-down capacity could unlock for your balance sheet? Try Participate’s ROI Calculator or request a demo to walk through a concentration-risk scenario with your team.