The Community Bank Leverage Ratio Final Rule: What It Means for Loan Participation and Syndication in 2026

Community banks entered 2026 facing a familiar balancing act: continue growing loans and serving relationship borrowers while managing tighter capital expectations, concentration risk, and operational strain. For many institutions under $10 billion in assets, that balancing act became even more complicated as CRE concentrations stayed elevated and lending standards tightened across the industry.

The Community Bank Leverage Ratio (CBLR) final rule, published in the Federal Register on April 29, 2026 and effective July 1, 2026, offers some relief. By lowering the leverage ratio requirement from 9% to 8% and extending the grace period from two quarters to four, regulators have given qualifying community banks more flexibility to keep lending through economic cycles. But flexibility is not the same thing as immunity.

In fact, the new rule may encourage more lending activity precisely when concentration risk is already a growing concern. That creates a strategic opportunity for banks that are prepared to use loan participations and syndications proactively — not reactively — as part of modern balance sheet management.

Key Takeaways

- The CBLR final rule improves lending flexibility for community banks. The revised 8% leverage ratio and extended four-quarter grace period reduce pressure on qualifying banks and create more room to support loan growth.

- Concentration risk remains a major issue despite the rule changes. The FDIC’s 2026 Risk Review still shows CRE concentrations near 300% of Tier 1 capital and reserves for many mid-sized institutions, meaning balance sheet pressure has not disappeared.

- Loan participation and syndication automation becomes even more strategic in 2026. Banks can continue serving borrowers, participate in larger relationships, and manage capital more efficiently by selling down portions of loans.

- Operational scalability matters as much as regulatory flexibility. Institutions relying on spreadsheets, email chains, and manual reconciliations may struggle to scale participation activity efficiently.

- Banks that modernize participation infrastructure now will be better positioned after July 1, 2026. The rule creates a narrow window to reassess concentration management, liquidity planning, and participation readiness.

Want to modernize how your institution manages participations and syndications? Explore how Participate helps banks automate loan participations, reduce concentration risk, and scale lending operations without adding headcount.

Learn more about the Participate loan sales ecosystem, read the Participate blog, explore the Loan Trading Network, or see how Capital Markets as a Service can help your institution move faster.

Understanding the Community Bank Leverage Ratio Final Rule

On April 29, 2026, the Federal Reserve, FDIC, and OCC published final changes to the Community Bank Leverage Ratio framework, effective July 1, 2026. The most notable change lowers the qualifying leverage ratio requirement from 9% to 8%.

The agencies also extended the CBLR grace period from two quarters to four quarters, subject to a limit of eight quarters in the previous five-year period. Under the revised framework, banks that temporarily fall below qualifying thresholds now have additional time to return to compliance before transitioning back to traditional risk-based capital standards.

However, the rule also clarifies an important threshold: if a bank’s leverage ratio falls below 7% during the grace period, the institution must comply with risk-based capital requirements.

For community banks, the changes are meaningful because the CBLR framework still requires qualifying institutions to maintain leverage ratios materially above many larger institutions operating under traditional risk-based capital rules. The updated framework gives banks more flexibility — but not unlimited flexibility.

According to the OCC, FDIC, and Federal Reserve, the changes are intended to reduce regulatory burden while preserving safety and soundness expectations for community banks. That balance matters because many institutions continue to face elevated portfolio concentrations and uncertain economic conditions.

Why the CBLR Final Rule Does Not Eliminate Concentration Risk

The new CBLR rule improves capital flexibility, but it does not solve the underlying portfolio concentration issues many banks already face.

The FDIC’s 2026 Risk Review highlighted that CRE loan concentrations for banks between $10 billion and $100 billion in assets remained at a median of 289% of Tier 1 capital and reserves, while the median was 311% for banks between $1 billion and $10 billion in assets. That is a significant exposure level for institutions already navigating higher funding costs, refinancing pressure, and uneven property valuations.

At the same time, the Federal Reserve’s April 2026 Senior Loan Officer Opinion Survey showed modest net shares of banks tightened C&I lending standards during Q1 2026. Banks cited:

- Stronger covenant requirements

- Higher collateralization expectations

- Increased pricing premiums on riskier loans

Those trends point to an important reality: even as regulators loosen one part of the capital framework, banks remain cautious about risk accumulation.

For many institutions, the danger is not simply regulatory compliance. It is operational and strategic concentration:

- Too much exposure to one borrower relationship

- Too much CRE exposure in one geography

- Too much capital tied to a handful of large credits

- Too little liquidity flexibility if markets tighten further

The result is that many community banks may have more room to lend under the revised CBLR framework while simultaneously facing greater pressure to actively manage portfolio diversification.

Loan Participation and Syndication Become More Important Under the New CBLR Framework

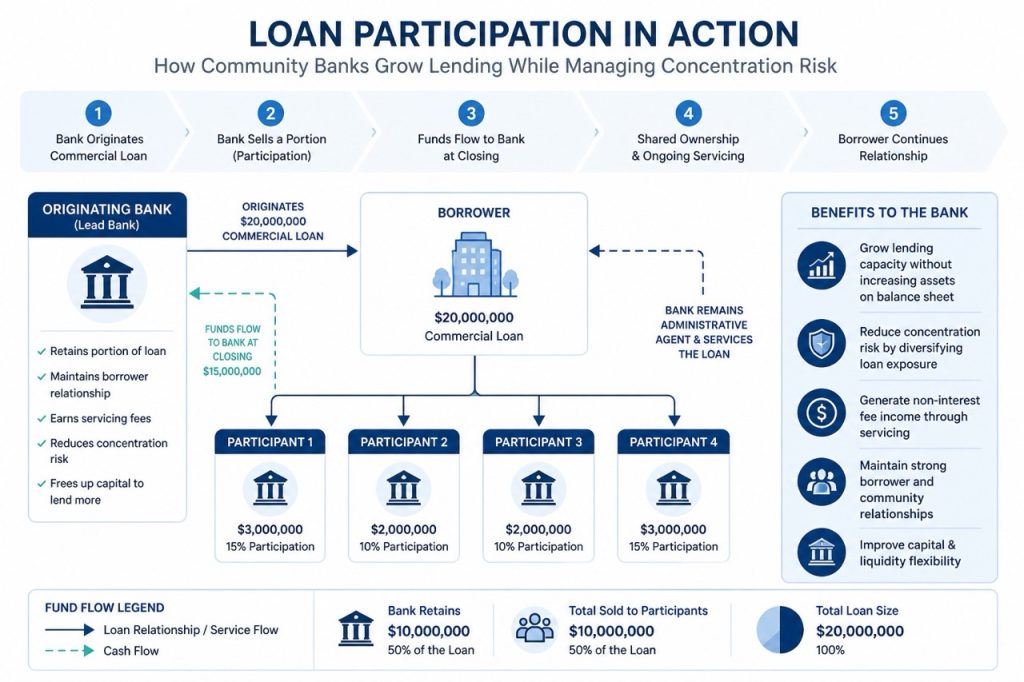

This is where loan participation and syndication become strategic tools rather than occasional transactions.

Historically, many community banks viewed participations as something to pursue only when a credit exceeded legal lending limits or created immediate concentration concerns. In 2026, that mindset is changing.

Banks increasingly use participations and syndications to:

- Preserve borrower relationships

- Continue originating larger loans

- Free Tier 1 capital capacity

- Improve liquidity flexibility

- Generate non-interest fee income

- Diversify loan concentrations proactively

Instead of saying “no” to a strong borrower relationship, banks can retain a portion of the loan while distributing exposure across trusted lending partners.

That approach becomes particularly attractive under the updated CBLR framework because the improved leverage treatment may encourage institutions to originate more loans. Without a participation strategy, however, additional loan growth can unintentionally increase concentration exposure.

As Participate notes in its industry materials, automation-driven participation platforms help banks keep lenders lending, reduce concentration risk, and increase fee income.

Participation Strategies Community Banks Should Revisit in 2026

1. Participating Out CRE Concentrations Earlier

Many banks wait too long before selling portions of CRE loans. By the time concentrations become uncomfortable, market appetite may already be constrained.

Banks should evaluate whether:

- Construction exposure is becoming too concentrated

- Geographic concentrations are increasing

- Certain borrower relationships are dominating the portfolio

- Participations can be arranged earlier in the underwriting process

2. Using Syndications to Win Larger Relationships

The revised CBLR framework may encourage more aggressive competition for larger commercial borrowers.

Syndications allow community banks to:

- Maintain lead bank relationships

- Retain servicing and treasury management opportunities

- Share exposure with peer institutions

- Compete more effectively against larger regional banks

3. Improving Liquidity Through Loan Sales

Selling portions of loans can improve balance sheet flexibility without fully exiting borrower relationships.

This matters as:

- Deposit competition remains elevated

- Funding costs remain volatile

- Liquidity management becomes more dynamic

- Loan demand continues unevenly across sectors

Operational Readiness Will Separate Leaders from Followers

Regulatory flexibility only creates value if a bank can operationalize it efficiently.

One of the largest barriers to scaling participations has historically been operational friction:

- Spreadsheet-based tracking

- Manual payment reconciliations

- Email document exchanges

- Delayed participant notifications

- Out-of-balance servicing records

Those workflows become difficult to sustain as participation activity grows.

Participate’s platform materials note that many institutions still rely on manual, spreadsheet-based processes that create scalability challenges as transaction volumes increase.

The institutions gaining an advantage are those automating:

- Loan sale workflows

- Participant servicing

- Funding requests

- Principal and interest disbursements

- Rate adjustments

- Shared balances and reporting

Participate describes this as creating a single system of truth for loan participations for originators and participants.

Why Automation Matters More in 2026

The combination of:

- Greater lending flexibility

- Persistent concentration pressure

- Tight staffing environments

- Increased scrutiny around operational controls

means banks cannot rely indefinitely on manual processes.

Automation allows institutions to:

- Scale participation volume without proportional staffing increases

- Reduce reconciliation risk

- Accelerate loan closings

- Improve transparency for participants

- Support audit and compliance readiness

According to Participate’s operational case study, automation reduced manual processing time by 70% while supporting more than 1,000 automated monthly transactions.

That operational leverage matters as banks prepare for the July 1, 2026 implementation timeline.

Community Bank Capital Management Is Becoming More Dynamic

The broader implication of the CBLR final rule is that community bank capital management is becoming more active and strategic.

Banks can no longer rely solely on:

- Static balance sheet assumptions

- Organic deposit growth

- Long-held portfolio concentrations

- Periodic participation activity

Instead, leading institutions increasingly view:

- Loan participations

- Syndications

- Whole loan sales

- Purchased loan automation

- Secondary market access

as core components of modern balance sheet strategy.

This shift is happening against the backdrop of continued banking consolidation. M&A activity continues targeting profitable, relationship-driven community banks, while many local markets remain fragmented enough to avoid formal concentration thresholds.

But regulatory concentration thresholds alone do not measure portfolio vulnerability effectively. Banks still need tools to actively manage:

- CRE exposure

- Industry concentrations

- Geographic risk

- Borrower-level aggregation

- Liquidity positioning

The revised CBLR framework creates more flexibility. It does not eliminate the need for discipline.

What Community Banks Should Do Before July 1, 2026

The implementation window creates an opportunity for leadership teams to reassess participation strategy before the rules take effect.

Immediate Action Items

Review concentration exposure trends

Evaluate:

- CRE concentrations

- Construction exposure

- Large borrower relationships

- Geographic concentrations

- Upcoming renewals and maturities

Assess participation readiness

Determine whether current workflows can support increased participation activity efficiently and accurately.

Evaluate operational bottlenecks

Identify:

- Manual reconciliations

- Spreadsheet dependencies

- Staffing limitations

- Delayed participant servicing processes

Revisit liquidity strategy

Assess how participations and syndications could support:

- Liquidity optimization

- Capital flexibility

- Fee income generation

- Relationship retention

Consider automation investments

Banks that modernize participation infrastructure now may gain a competitive operational advantage over institutions still relying on fragmented workflows.

Frequently Asked Questions

What is the new community bank leverage ratio requirement for 2026?

The final rule lowers the qualifying CBLR requirement from 9% to 8%, effective July 1, 2026.

What happens if a bank falls below the CBLR threshold?

Banks now receive a four-quarter grace period to return to compliance, subject to a limit of eight quarters within the previous five-year period. However, if the leverage ratio falls below 7%, the institution must comply with risk-based capital requirements.

How do loan participations help manage concentration risk?

Loan participations allow banks to sell portions of loans to other institutions while retaining borrower relationships, reducing exposure tied to individual loans, industries, or geographies.

Why are community banks focusing more on syndication in 2026?

The revised CBLR framework may encourage additional lending activity, making syndications an effective way to support larger relationships without overextending concentration exposure.

How does automation improve loan participation operations?

Automation reduces manual reconciliations, improves reporting accuracy, accelerates closings, and helps banks scale participation activity without significantly increasing operational staffing.

Conclusion

The 2026 CBLR final rule is a positive development for community banks. Lower leverage requirements and longer grace periods create meaningful flexibility for institutions focused on relationship lending and growth.

But flexibility alone does not solve concentration risk.

If anything, the revised framework may accelerate loan growth at a time when CRE exposure, liquidity management, and operational efficiency remain critical concerns. Community banks that proactively strengthen participation and syndication capabilities will be better positioned to grow safely while preserving capital flexibility.

The institutions that win in this environment will not simply lend more. They will manage balance sheets more dynamically, automate participation workflows more effectively, and use loan sales strategically to keep lenders lending.

To learn how Participate helps financial institutions automate loan participations, reduce concentration risk, and scale lending operations efficiently, visit ParticipateLoan.com or explore more Participate insights.